Wynn Resorts seems to be doing pretty well. However, a recent analysis by Valens Research suggests that the company could be in more trouble than the stock price suggests.

Joel Litman is the Chief Investment Strategist for Valens, a global equity and credit research boutique that serves 200 of the 300 largest institutional investors, and thousands of family investors. In a recent article, Litman analyzed the post-pandemic optimism that has driven Wynn Resorts' stock price from its five year low of $51.97 in May 2020 to $128.39 on June 4, 2021.

Litman explains why in an article for the Altimetry Daily Authority. "Folks are expecting these casino companies will take off as people get back to normalcy."

Most of that rise came in early-2021. Through January of 2021 Wynn's stock price hovered between $99 and $106 per share. From Feb 1, 2021 onwards, it has been on a sharp climb gaining 37.5% to hit $140.00 on March 17. It's lost a little weight since then, but is still worth around 20% more than its price on New Year's. This reflects 2021's slow move towards normalcy and herd immunity.

In the rest of his piece, Litman urges caution.

"With the market excited about a return to normalcy, investors are pricing returns to surge to 11%. Based on pre-pandemic performance, this doesn't look reasonable," Litman writes.

Litman calls out the way Wynn trod water during the pandemic. "Nothing has changed about Wynn's operations since before the pandemic. It still operates the same lavishly appointed casinos… And it hasn't moved aggressively into online sports betting, iCasino gambling, or any other potential strategy to transform the business."

While poker players probably don't need to start worrying about losing the poker rooms at the Wynn and Encore in Vegas, anyone with stock in Wynn might want to call their broker.

Can't Wynn for losing

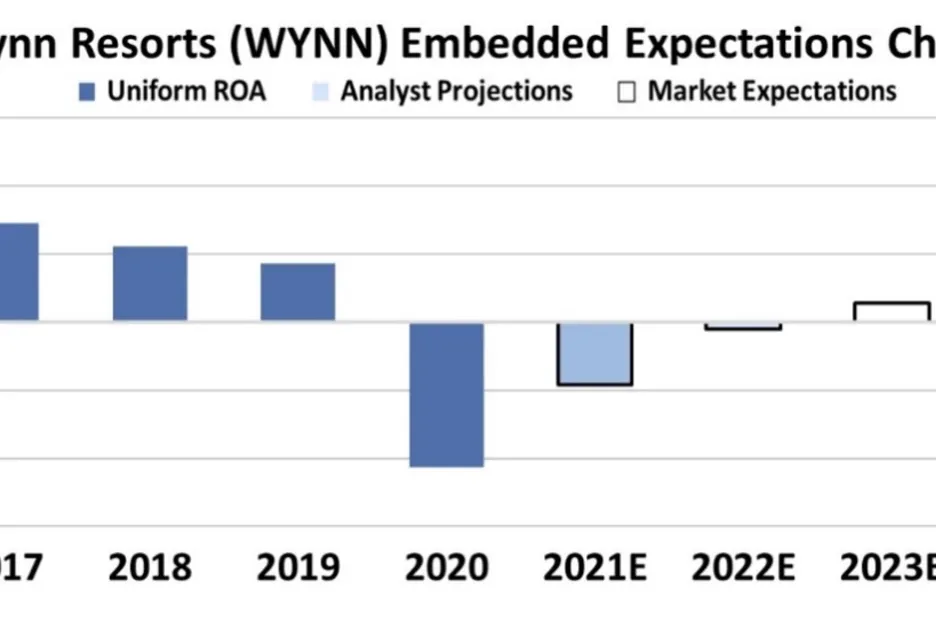

Valens uses accounting methods to break down company balance sheets and translate them from the standard U.S. accounting practice of Discounted Cash Flow modeling to its own Uniform Adjusted Financial Reporting Standards.

The idea is that the DCF model allows companies to hide aspects of their financial health by using malleable assumptions about the company's future. UAFRS strips back these accounting tricks to give a better picture of a firm's actual current financial state.

Though things are looking up for the casino industry as a whole, Wynn may not be getting to enjoy all the perks. Its Vegas poker rooms are doing well, and the Wynn Summer Classic is well under way. But in the company's non-Vegas holdings things are a bit more up in the air.

The Encore Boston Harbor has already said it won't be laying on poker until 2022 at the earliest. It has to focus on the more profitable aspects of its business to stay viable. That means slots and table games. This tightening up seems to support the story that Litman tells.

Using UAFRS, Valens predicts that 2021 will show a Return On Assets of around -5% (see the graph above, taken from Litman's article with permission). In 2022, Valens' expectations are a little better but still have Wynn's ROA in the red. Only when they start looking at market expectations for 2023 does Wynn start to show a positive ROA.

So things are not all doom and gloom.

However, Wynn is likely to lag behind some of its faster-moving and/or better-established competitors. Especially those companies like MGM and Caesars that have diversified businesses that include online casinos, sportsbooks, and poker rooms.

Featured image source: Flickr by Saguro